Oregon CHIPS at a Crossroads:

A New Statewide Semiconductor Ecosystem Assessment

By Damon Runberg – Business Oregon Economist. • June 30th, 2026

Oregon’s semiconductor industry has long been one of the state’s greatest economic assets anchoring tens of thousands of high‑wage jobs, driving billions in exports, and forming the backbone of the Silicon Forest. Over the past few years, the state has administered incentives such as the Oregon CHIPS Fund and the R&D Tax Credit for Semiconductors to help fuel growth of a sector so critical to Oregon’s economy. However, Oregon’s semiconductor industry now sits at a pivotal crossroads according to a new study by the University of Oregon’s Institute for Policy Research and Engagement (IPRE) prepared for Business Oregon and Oregon State University.

Oregon’s semiconductor ecosystem remains strong today, but its long‑term growth and competitiveness are increasingly fragile. The industry is experiencing a sustained growth spurt driven by AI infrastructure buildout and the increasing ubiquity of microchips in consumer, industry, automotive, and healthcare markets – and other states are aggressively competing for this growth. Without strategic action, the Oregon risks losing ground in an industry projected to surpass $1 trillion globally by 2035. Let’s look at some of the key insights from the report and what they mean for Oregon’s economic future.

Oregon should treat the Silicon Forest as a strategic policy priority, not just an industrial asset. It is where the industry advances the transistor architectures, wafer processes, and packaging technologies. It is the epicenter of Moore’s Law, and influences not only Oregon’s economy but also the future direction of the global semiconductor industry. Simply supporting and sustaining this core is insufficient; it must be nurtured and encouraged to ensure that Oregon stays relevant in the next generation of semiconductors.”

—Scott Mokler,

Technical Advisor to the Oregon Semiconductor Talent Consortium and former Intel Senior Principal Engineer

A Legacy of Strength, But Not Enough to Guarantee the Future

For nearly 50 years, Oregon has been home to one of the most established semiconductor clusters in the world. The region’s deep engineering expertise, strong research institutions, and dense supplier networks set it apart. Additionally, semiconductor firms described Oregon’s workforce as highly capable, with exceptional “social capital.” This reflects the deep institutional and technical knowledge of the state’s workforce. For a highly technical industry, it might be surprising to hear that human relationships are one of the most important strengths for the sector. A good example is the level of engagement of retired experts, many of which continue to support the industry through mentoring and consultation.

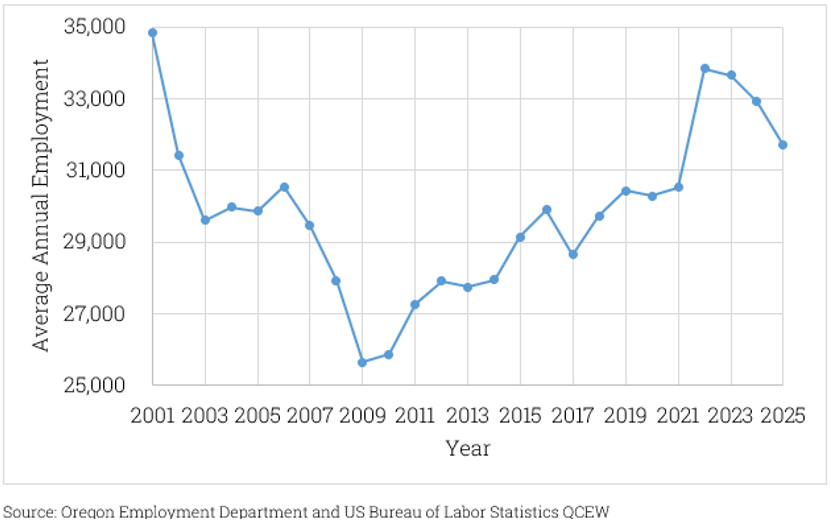

But the report warns that these advantages are no longer sufficient on their own. In 2025, the industry shed over 3,000 jobs (-9.5%), mostly tied to announced layoffs at Intel. The report found that other states, notably Arizona, Texas, and New York, are aggressively recruiting semiconductor companies, assembling large incentives, shovel‑ready industrial sites, and coordinated talent pipelines. Oregon is no longer competing just on the expertise of its semiconductor workforce, but is increasingly competing against places offering faster speed of development, more predictable regulatory environment, and lower costs.

Intel’s presence is foundational to Oregon’s semiconductor industry as a legacy business and the state’s largest private sector business. Its R&D footprint and supplier gravity shape a huge part of the regional ecosystem. But this reliance exposes Oregon to volatility. Recent workforce reductions and shifting corporate strategies illustrate the risk: when Intel contracts, the company’s suppliers downsize too. And interviewees across the report noted that new Intel expansions are increasingly occurring in other states, not Oregon. While this doesn’t mean that Intel is leaving, it means Oregon must diversify the semiconductor ecosystem if it wants long‑term stability.

The global semiconductor industry is expanding faster than at any point in history, driven by AI, automotive electrification, cloud computing, and advanced packaging. Oregon has a real opportunity to capture some of this growth, but the competition is intense.

Interviewees consistently flagged four barriers holding Oregon back in this battle for semiconductor industry investments:

Limited industrial land: no sites available of 1,000+ acres, unlike Ohio or Arizona.

Rising costs and regulatory uncertainty: This is leading firms to site expansions out of state.

Electrical grid constraints: A looming challenge for fabs, data centers, and suppliers.

Workforce shortages: Particularly challenging to hire technicians and mid‑career talent, although this is less of a barrier now after recent layoffs.

While Oregon universities produce excellent engineers, the scale of its higher‑education system is small compared to competitor states. Technician shortages are acute, and too few Oregon students are entering STEM pathways.

Interviewees also emphasized an additional often overlooked barrier, Oregon’s reputation. Historically, Oregon’s high quality of life has been a competitive advantage for attracting workers, yet concerns about cost of living, taxes, and perceptions of Portland deter many would‑be recruits. These barriers put the industry at a high risk of stagnation if we continue to pursue the status quo.

Recommendations from the Report

The report sends a clear signal that Oregon has many of the assets needed to remain a semiconductor powerhouse, but that growth will not happen automatically. The next decade will be decisive. The study outlines the following set of policy and programmatic actions designed to stabilize and grow the industry.

- Support Small and Mid‑Sized Firms: These firms form the backbone of the supply chain but struggle to compete with Intel for talent and capital. Targeted incentives would help diversify the ecosystem and reduce risk.

- Expand Industrial Land and Infrastructure: Oregon must prepare large, development‑ready industrial sites paired with power, utilities, and expedited permitting to compete for future investments.

- Strengthen Oregon’s Business Climate: Companies report feeling uncertainty around taxes, regulations, and state‑level support. More predictable policies could help restore confidence and prevent future expansions from drifting elsewhere.

- Build a Unified, Statewide Talent Engine: FAST (Frontiers of Advanced Semiconductor Technology), a statewide collaborative to support and grow the industry, offers a promising foundation. But scaling this partnership and landing federal investment through the National Science Foundation (NSF) Regional Innovation Engine Program will be critical in addressing workforce challenges.

- Mobilize Oregon’s Semiconductor Retiree Network: Oregon’s deep bench of experienced professionals is a unique competitive advantage. Formalizing these networks could boost mentoring, innovation diffusion, and talent development.

Oregon can remain a global leader in semiconductor R&D with coordinated action around land, infrastructure, workforce, incentives, and improving the business climate. But with other states staying focused on attracting industry investment during this time of growth, this report finds that Oregon needs to go beyond the status quo to compete. Without the public sector taking additional action, there is a real risk of the state slowly losing ground as new investments and expansions flow elsewhere.